.jpg)

For years, digital growth in the financial sector has been measured through visible and easily reported metrics: app downloads, new account registrations, customer acquisition costs, media reach, and website traffic. These numbers have traditionally been viewed as indicators of growth and market success. More downloads meant more users. More registrations meant stronger growth. More traffic suggested greater demand.

For years, digital growth in the financial sector has been measured through visible and easily reported metrics: app downloads, new account registrations, customer acquisition costs, media reach, and website traffic. These numbers have traditionally been viewed as indicators of growth and market success. More downloads meant more users. More registrations meant stronger growth. More traffic suggested greater demand.

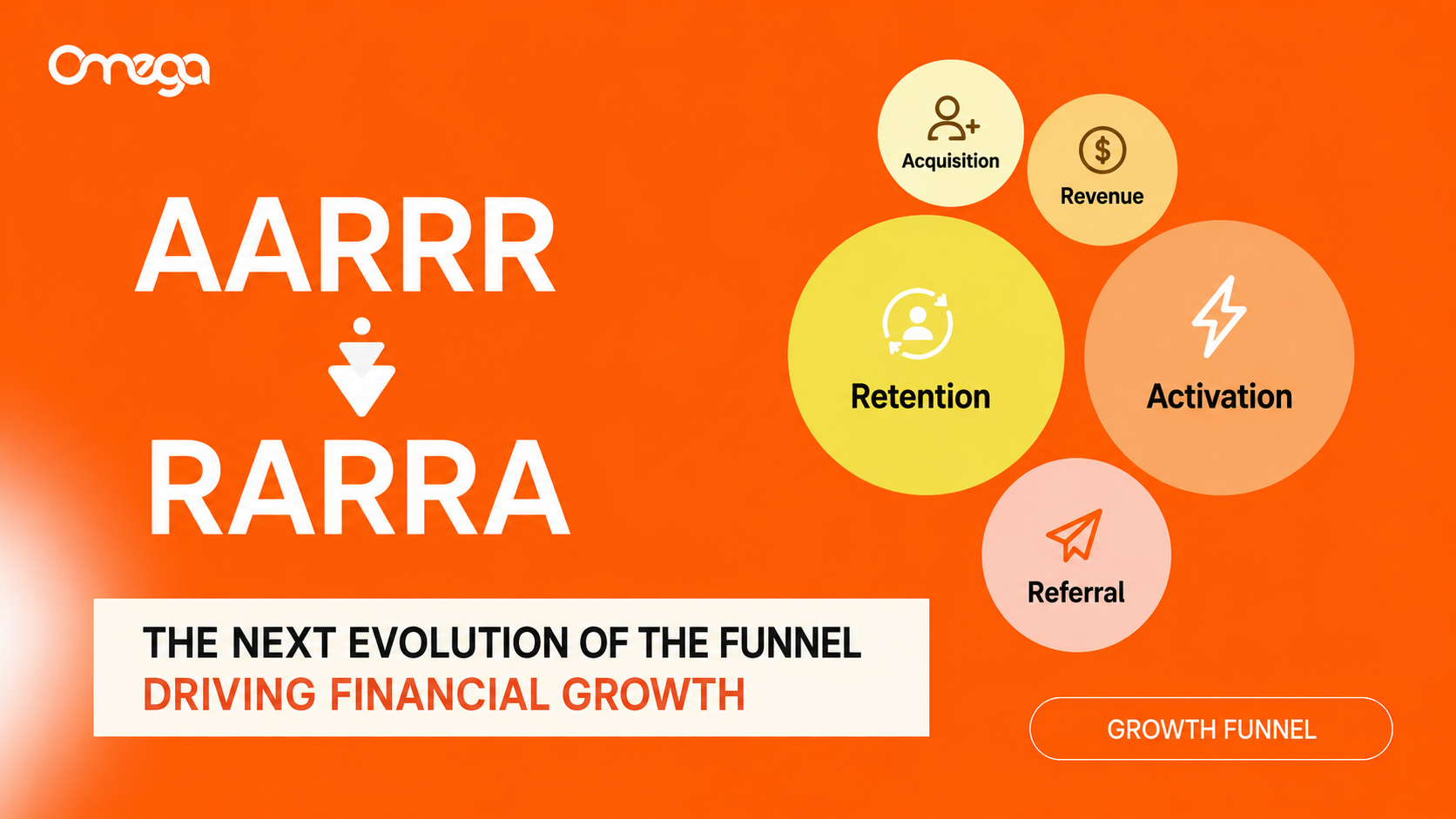

However, as the financial industry enters the Mobile Banking 2026 era, these metrics alone are no longer enough to reflect the true health of a business. Many financial institutions are discovering a difficult reality: the more budget they invest in acquiring users, the weaker their growth foundations can become if those users fail to engage, return, or generate long-term value. This is why the shift from AARRR to RARRA has become one of the most important transformations in modern financial growth strategy.

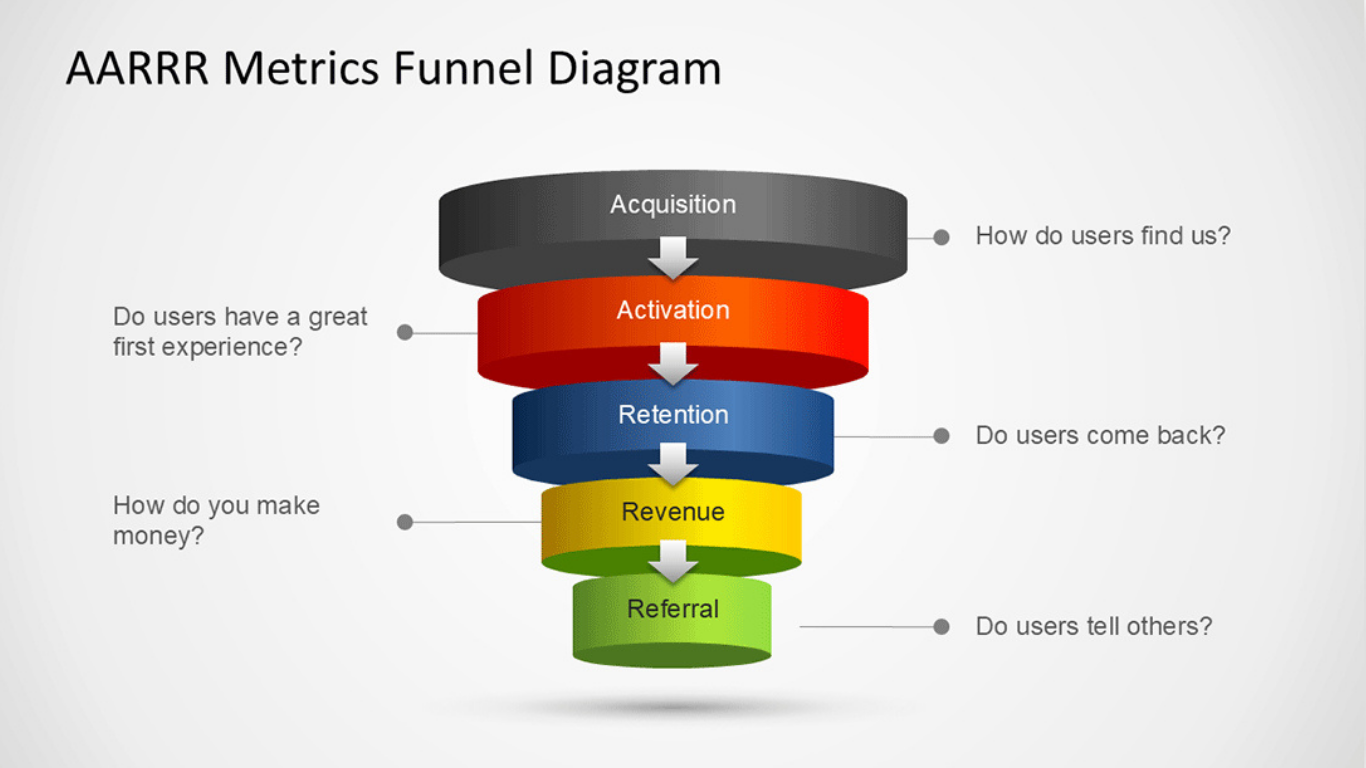

1. What is the AARRR growth framework?

AARRR is a growth framework consisting of five stages: Acquisition → Activation → Retention → Referral → Revenue

The model begins with acquiring users, then activating them, retaining them, encouraging referrals, and finally generating revenue.

For many years, AARRR served as one of the most widely adopted frameworks in growth marketing because it provided a structured way to analyze the customer journey.

Businesses could systematically answer key questions:

- How are users finding us?

- Are they experiencing value quickly?

- Do they return?

- Will they recommend us?

- Are they generating revenue?

For many digital products, this framework remains highly effective. However, within financial services, particularly mobile banking applications, placing Acquisition at the beginning of the funnel can create a significant strategic blind spot.

Organizations become obsessed with increasing downloads, opening new accounts, and lowering acquisition costs. Meanwhile, the most difficult challenge remains largely unresolved:

How do you make users trust the platform, use it consistently, return regularly, and integrate it into their financial lives?

This is where AARRR begins to show its limitations.

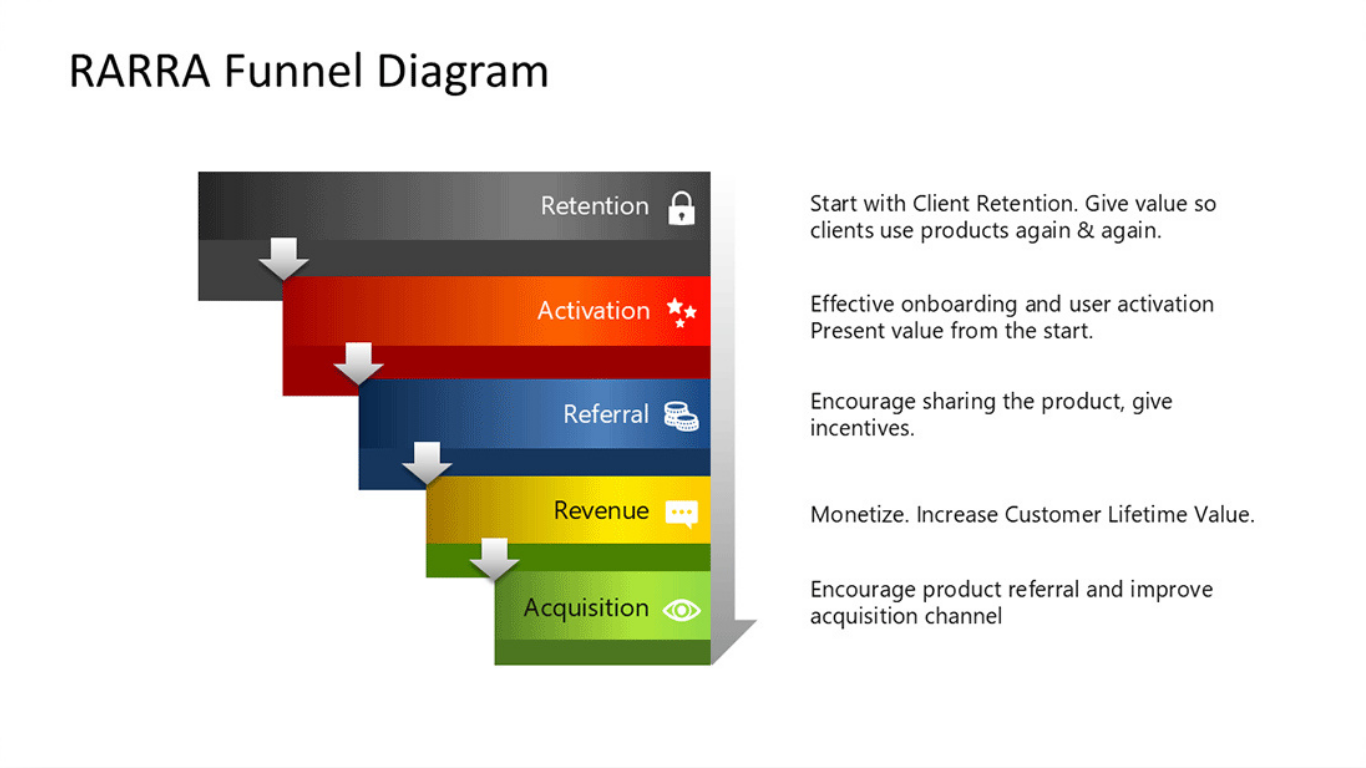

2. What is the RARRA growth framework?

2. What is the RARRA growth framework?

Unlike AARRR, the RARRA framework places Retention at the beginning of the growth journey.

The sequence becomes:

Retention → Activation → Referral → Revenue → Acquisition

The framework starts with a simple but powerful question: "Is the product valuable enough for existing users to come back?"

For financial institutions, this shift is profound. A banking application does not win simply because someone downloads it.

It wins when users return to:

Transfer money

Pay bills

Check balances

Manage spending

Receive personalized offers

Save money

Invest

Access additional financial services

If users do not come back, acquisition spending simply accelerates leakage within the funnel.

RARRA forces organizations to focus on the quality of engagement before scaling acquisition efforts.

Businesses begin asking: "Why aren't our current users staying?"

That change in perspective often reveals far more growth opportunities than another advertising campaign.

3. The financial industry context: Growth is becoming more expensive

3. The financial industry context: Growth is becoming more expensive

The Mobile Banking 2026 landscape presents a challenging reality. Growth in financial services is becoming increasingly expensive, more competitive, and significantly harder to sustain. Many financial institutions initially focused heavily on user acquisition.

Downloads increased.

Registrations increased.

Campaign reports looked promising.

However, deeper analysis of customer journeys, particularly around eKYC (electronic Know Your Customer) processes, revealed major inefficiencies.

According to performance marketing report conducted by Omega Media, the cost of acquiring a new financial services user can range from approximately 120,000 to 300,000 VND per user. At the same time, completion rates from registration to successful identity verification often range between only 60% and 70%. This means a substantial portion of marketing investment disappears before users even enter the product ecosystem.

Users abandon onboarding journeys for many reasons:

Lengthy registration processes

Friction-filled user experiences

Complex verification requirements

Lack of immediate value perception

Interrupted onboarding flows

The challenge is no longer simply a media efficiency problem. It is a growth system problem. Acquisition can only be effective when the rest of the journey works.

4. Why Financial Institutions Need to Move from AARRR to RARRA

Financial organizations need to shift toward RARRA because acquisition is no longer a sustainable starting point when retention remains weak. Under the traditional AARRR mindset, companies invest heavily at the top of the funnel.

Budgets flow into:

Advertising campaigns

User acquisition programs

App install campaigns

New account registrations

This approach can produce rapid short-term growth.

However, in Mobile Banking, a newly acquired user only becomes valuable when they successfully complete onboarding, finish identity verification, adopt core product features, and continue using the application over time. If eKYC completion rates remain low, if users open the app once and never return, or if they fail to discover meaningful value, acquisition stops being growth. It becomes cost. RARRA forces organizations to reverse the problem.

Instead of focusing on bringing more people into the system, companies focus on creating experiences that encourage users to stay. This represents a shift from budget-driven growth to experience-driven growth. And in the financial sector, experience is increasingly becoming the ultimate competitive advantage.

5. How financial institutions can succeed with the RARRA model

5.1 Retention: The new foundation of Mobile Banking growth

In mobile banking, retention is no longer just another post-campaign metric. Retention is the foundation upon which sustainable growth is built. A successful banking application appears at exactly the right moment in a customer's life.

That might mean:

Reminding users about upcoming utility payments

Alerting them to unusual spending behavior

Recommending personalized savings plans

Delivering relevant cashback offers

Suggesting financial products aligned with their goals

When users feel understood, they have a reason to return.

When they return consistently, activation becomes easier.

When experiences are positive, referrals become natural.

When trust grows, revenue follows.

Retention is no longer the result of growth.

It is the starting point.

5.2 Brandformance: Communicating effectively with Gen Z consumers

Traditional financial advertising messages such as: "Download the app now", "Open an account today" and "Claim your reward immediately" are becoming increasingly ineffective, especially among younger audiences. Gen Z consumers have more choices than ever before. They are less responsive to direct promotional messages and more likely to engage with brands that understand their lifestyles and aspirations.

According to Omega Media's strategic approach, one of the most effective solutions is Brandformance. Brandformance combines brand building with performance-driven outcomes.

Rather than focusing exclusively on features and promotions, financial brands should tell stories that connect with real-life situations.

Examples include:

Managing spending at the end of the month

Splitting bills with friends

Budgeting for travel

Earning cashback on everyday purchases

Building sustainable saving habits

When content feels relevant, relatable, and useful, customers do not feel like they are being sold to.

They feel understood.

And understanding is often the first step toward trust.

5.3 AI: The ultimate personalization engine

Every banking customer behaves differently. Some users travel frequently. Others spend heavily on shopping. Some focus on savings. Others seek investment opportunities. Many simply want better visibility into their daily finances. Creating individualized experiences manually is nearly impossible at scale. Artificial Intelligence changes that. AI enables financial institutions to:

Detect behavioral patterns

Predict customer needs

Personalize recommendations

Customize app interfaces

Deliver timely and relevant communications

A frequent traveler may receive travel-related offers.

A shopping enthusiast may receive cashback recommendations.

A user with recurring payments may receive proactive reminders.

A customer with stable cash flow may receive investment or savings suggestions.

The result is a banking experience that feels relevant, useful, and frictionless.

Instead of overwhelming users with generic messages, AI helps deliver the right message to the right person at the right moment. This is where retention, personalization, and growth begin to converge.

Conclusion

Conclusion

Effective growth is no longer about manipulating surface-level metrics. It is about understanding the customer journey deeply, identifying friction points, and systematically improving every interaction within the growth ecosystem. The rules of financial growth in 2026 are becoming increasingly clear. The winners will not necessarily be the organizations spending the most on acquisition. They will be the organizations that understand customers best, build stronger retention loops, personalize experiences effectively, and know exactly when to accelerate growth. For financial institutions, the future lies in moving beyond acquisition-first thinking and building growth systems powered by retention, customer experience, data intelligence, and personalization.

.png)